← Back to the Alcohol.law Digest

Changes to Federal Excise Tax Bond Requirements – Do You Still Need a TTB Bond?

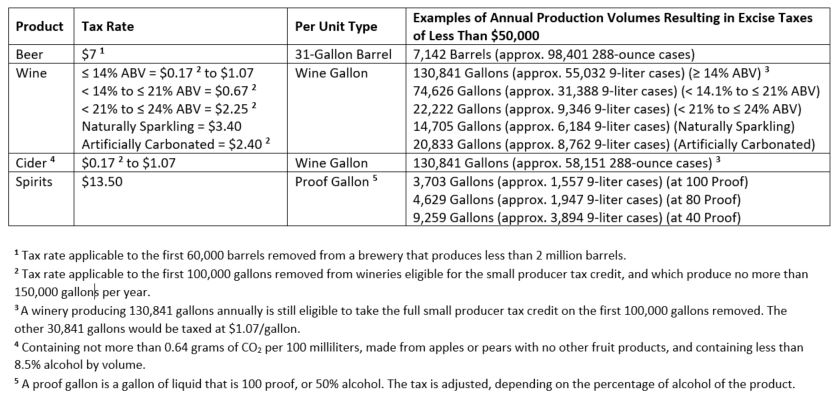

The Protecting Americans from Tax Hikes Act (the “PATH Act”) took effect on January 1st, 2017. The PATH Act changes the bond requirements for some TTB-permitted producers that are liable for excise taxes on distilled spirits, wine, and beer. Currently, all producers are required to file a bond covering operations and withdrawals of spirits, wine, and beer. The PATH Act provides that producers that reasonably expect not to owe more than $50,000 in excise taxes during the year are no longer required to have a bond on file with the TTB. Beginning this year, a new applicant that indicates that they do not expect to owe more than $50,000 in excise taxes during the first calendar year will not be required to submit a bond with the permit application. Also, an existing producer may request termination of its bond requirement by filing an amendment to its permit, which the TTB will process only after the producer has submitted excise tax returns, payments, and reports for 2016, so that the TTB can determine the producer’s eligibility to terminate its bond. The chart below provides examples of production volumes that would result in annual excise taxes of less than $50,000, meaning that producers under those volumes would not be required to file a bond with the TTB covering operations.

The TTB has issued Industry Circular 2016-2 with more information, and will publish regulations to implement the above statutory changes in the near future. For more information regarding the PATH Act and TTB bond requirements, contact one of the attorneys at Strike Kerr & Johns for further guidance.

Browse all tags: